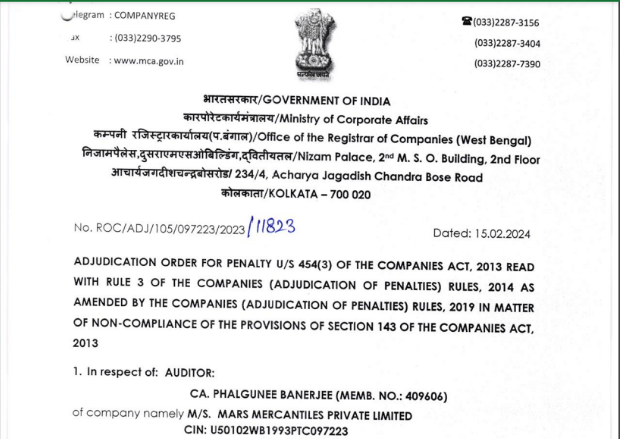

Through its Gazette Notification No. A-420a / i 12/2014-Ad.II areas 24.03.201, the Ministry of Corporate Affairs To determine penalties under the terms of this Act, S appoints an undersigned officer as an adjudicating officer. This officer will exercise the powers granted by section 454(1) of the Companies Act, 2013 (henceforth referred to as the Act) read in conjunction with the Companies (Adjudication of Penalties) Rules, 2014. Entrusted with deciding fines under section 143 of the Companies Act, 2013, is the undersigned.

WHEREAS Mars Mercantiles Private Limited (hereinafter referred to as the “Company”) is a registered entity incorporated on 11th June 1993 under the provisions of the Companies Act, 1956, with its registered address at 175, Karnanni Estate, 209, A J C Bose Road, Kolkata, WB 700017, India, as per the MCA website.

1) Based on an Inquiry Report conducted under Section 206 of the Companies Act, 2013, the following instances of violations have been identified:

Schedule III of the Companies Act, 2013 stipulates that a company should disclose additional information regarding aggregate expenditure and income on items exceeding one percent of revenue from operations or Rs. 1,00,000, whichever is higher. This includes interest expense.

The company’s Financial Statements for the period from the financial year 2015-16 to 2019-20 have recorded the following income or expense: [Please provide specific details of income or expenses for this period.]

/e/ In the auditor’s opinion, whether the financial statements comply with the accounting standards;

(g) Whether any director is disqualified from being appointed as a director under

(h) Any qualification, reservation, or adverse remark relating to the maintenance

of accounts and other matters connected therewith.

(j) Any other matters as may be prescribed.

For all the instances listed in the table above, under Rule 3(12) of the Companies (Adjudication of Penalties) Rules, 2014, and the proviso of the said Rule, as well as Rule 3(3) of the Companies (Adjudication of Penalties) Rules, 2014, regarding the above violations.

Your attention is also drawn to section 454(8) of the Act concerning the consequences of non-payment of the penalty within the prescribed time limit of 90 days from the date of receiving a copy of this order.