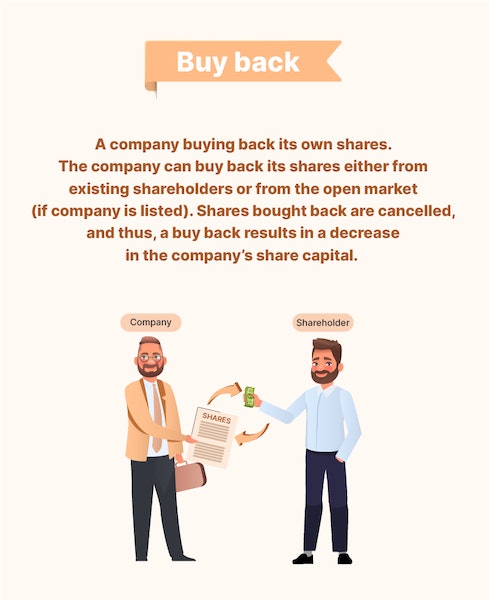

A company purchasing its own stock is called buy back.

Most often, companies buy back shares:

a. To decrease the number of outstanding shares in the hands of investors. To increase promoters’ shareholding (since shares bought back are cancelled)

b. To increase earnings per share (if a company’s earnings are the same, buy back of shares reduces the number of shares issued)

c. To pay surplus cash to shareholders when the company does not need it for its business

d. To reward shareholders by buying back of shares at a substantially higher price than market price

e. To support share price on stock exchanges if company management thinks that the share price is less than its worth

There is a limit to how many shares can be bought back during a financial year, and only a company with sufficient cash (in free reserves or in its securities premium account) can do so.